Part one of a three-part series on Developing a Lean Quoting Process.

Part 2: “Creating a Lean Quoting Process to Support Your Lean Transformation” details the part of the process that moves most quotes quickly through to completion.

Part 3: “How a Lean Quoting Process Helps You Capture High-Value Opportunities” describes how setting up a Daily Opportunity Review Board helps your company strategically respond to high-value customer inquiries.

**********

Have you implemented lean at your facility and are wondering, “We have made all of these improvements: faster flow, better quality, improved employee engagement, and increased on-time delivery. Why don’t the results show up on the Profit and Loss statement?” This is a common question within companies early (and sometimes later) in their lean journey.

You may have realized some minor cost improvements using attrition to assimilate the excess employees. But you haven’t seen the large-scale profit improvements. There is a simple reason for that. A true lean transformation is not a cost-cutting exercise; it is a culture change first and foremost. It is respect for your employees, so they are not worried about their jobs disappearing, and are challenged to be the best they can be. After that, a lean transformation is a growth strategy. You need to use the freed up capacity to GROW the business systematically and strategically. The real benefit to the lean P&L is to allow you to sell more with the same workforce and equipment.

What are your biggest expenses? Usually, it is materials, depreciation, labor and fringe benefits, utilities, and supplies. The only real variable costs are material content and a few supplies. Your depreciation does not change just because you have improved flow time by 75%. You might see a reduction in overtime each month from efficiency gains; otherwise, your labor will only change if you reduce the employees you redeploy due to productivity gain. But doing that will stifle your lean deployment. If there is attrition, you can avoid hiring by redeploying employees. But again, these are not huge savings. Most of your utility expense is for either heating or cooling the facility. Therefore, the only utility savings comes from running equipment less, which is minimal from a financial impact.

Your lean activities also pull capitalized labor and overhead from the balance sheet to the income statement as your customers realize that you are delivering product faster. While this is good, they will realize that they do not have to order so far in advance nor keep as much inventory on hand. You may see a short-term sales drop because your customers will start depleting their excess inventories without reordering. After all, they know you can deliver faster.

Lean Transformation as a Growth Strategy

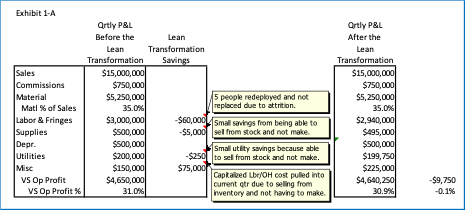

In Exhibit 1-A, you can see the impact on the value-stream income statement and see why top management might not be able to understand all the excitement on the floor about the improvements from all the lean efforts.

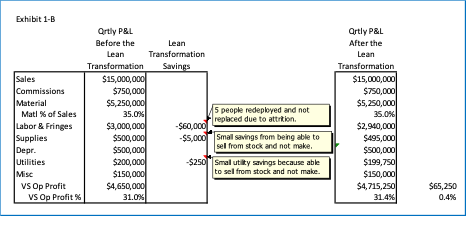

If this were all you had to look at, you would not want to go any further with lean. Sales have stayed the same. Your profits have decreased in dollars and as a percent of sales. Even if you removed the impact of pulling into the quarter the capitalized labor and overhead from prior quarters sitting in your inventory, Exhibit 1-B shows that the effect is minimally favorable. Here you see that we only added $65,250, or 0.4%, to the bottom line for all our effort.

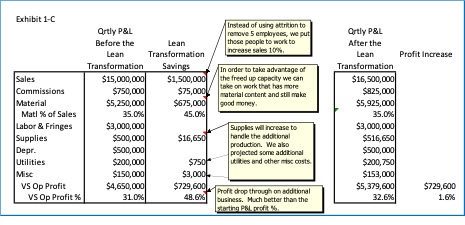

Let’s look at the income statement where instead of reducing the labor to sell the same amount of product, we use the freed-up capacity to sell more product strategically. You can see the impact is shown in Exhibit 1-C.

Gaining the ability to sell more with less labor is the real power of lean as a strategy! We improved our profit margin by 1.6% points and $729,600. In our analysis, you will note that we acknowledged we could selectively and strategically go after business more aggressively. A slightly lower selling price will create a higher material content percentage (35% to 45%). Because we utilized our excess workforce capacity to sell more with the same number of employees, we were able to make a significant improvement in our profits. Using lean as a growth strategy, using your freed-up capacity, is the most effective way to take advantage of your lean improvements.

Lean Transformation’s Affect on the Balance Sheet and Cash Flow

Thus far, the discussion has been around the strategic issues as they relate to the Profit and Loss statement. Another area in which lean impacts the financial statements is on the balance sheet and cash flow statements. For the balance sheet, you will see a lowering of all three components of inventory – raw material (RM), work-in-process (WIP), and finished goods (FG). You will see a decrease in FG because you will need less in stock since you can replenish your FG inventory faster. You will also see a lowering of WIP inventory because your product is moving through the plant much more quickly and not sitting nearly as long. This is partly because it is flowing faster but also because you would have instituted Standard WIP (SWIP), which controls the amount of inventory allowed on the floor between successive operations. Finally, you will need less raw material in stock because you can schedule the receipt of the raw material in smaller quantities and more frequently due to the speed of product flow.

Because you will have less money invested in your inventory, the line of credit you utilize to manage your business will be lower, reducing your interest expense. Finally, you will have improved cash flow as you sell more and tie up less money in inventory. This outcome is critical to a growth strategy since now you have more cash available for capital expenditures if needed, or for other investment opportunities.

Despite these critical balance-sheet and cash-flow benefits, too many managers/general managers/presidents fixate on the impact on the income statement. As noted earlier, until you properly utilize your excess capacity to build and sell more product, the benefit to the income statement is minimal at best.

So why are customers not flocking to you with new business? You are delivering faster and with better quality. They get their product on time and can reduce their in-house inventory. You would think that you would be flooded with new opportunities and win many more quotes.

The Missing Piece: Fixing the Quoting Process

So far, your lean activities have attacked the plant floor but not the quoting process. How do you change the whole quoting process to be nimbler, thereby allowing the company to process and win more quotes at the margins desired? You cannot continue to use standard cost thinking, silo activities, and linear processes to accomplish the growth that lean promises. Just like leaning out the factory floor, you must lean out your quoting processes to utilize the capacity gains your other lean efforts have garnered. In a subsequent article, I will discuss a unique quoting process that will allow you to quote faster and free up quoting resources to spend the appropriate amount of effort on the few key quotes that can drive your profits higher.