“Lean Accounting” has been around for about 30 years, yet its adoption has not been widespread. Is that true?

When those of us that have been involved in lean accounting for a long time try to convince other financial executives to adopt it, the response we get is generally along the line of “we have to follow GAAP accounting and can’t do lean accounting”. As Jim Womack has regretted using the word “lean” to describe the concepts, principles and practices of Toyota’s business, so have I come to regret the adoption of the phase “lean accounting” because it implies that it is an alternative to Generally Accepted Accounting Principles (GAAP).

But it’s not.

The first thing to understand about accounting is that there are multiple sets of requirements that serve different purposes. For example, GAAP sets out the requirement for financial statements provided to shareholders, creditors, the Securities and Exchange Commission (SEC), and other public reporting in the U.S. The Internal Revenue Service sets out the requirements for financial reporting used to determine tax liabilities. Government Cost Accounting Standards (CAS) set out the requirements for providing financial information for government procurement contracts. International companies follow the International Financial Reporting Standards (IFRS). In addition, there are different accounting standards for specialized organizations, such as not-for-profit, government, etc. Another type of financial statements that companies use are Managerial Accounting Statements which are intended to help management better understand their business.

When we talk about Lean Accounting, we are talking about Managerial Accounting…sometimes called Management Accounting. Whereas the other forms of accounting must comply with requirements established by parties outside of the company, management accounting does not have this constraint. Since its use is not intended for external users, it can be adapted to the needs of its intended users…management. As a result it can be different for different companies and different industries. It is whatever management deems it to be in order to help it understand the business better and make better decisions.

The other aspect of Lean Management Accounting is that it is comprised of two subsets. The first is applying the concepts, principles and practices of Lean to the company’s business and accounting processes. Since one of the goals of Lean is to reduce the amount of time it takes to do everything by eliminating activities that do not add value (i.e. waste), it would not be unreasonable to call this subset “lean accounting”. The other subset encompasses the information that is provided to management in the form of metrics and financial statements. This subset is usually referred to as “accounting for lean”.

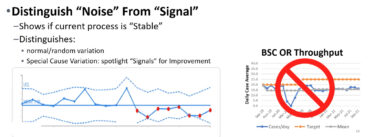

All companies use metrics. The most important thing to understand about metrics is that they have to support the company’s strategy. Since Lean Strategy is very different from Traditional strategy, many of the metrics that a company should use when implementing a Lean Strategy are very different from those that have been used before. An analysis of the company’s metrics must be made in order to determine which of the existing metrics will support the new Lean Strategy, which can be modified to do so, which do not and must be discontinued, and which new ones should be adopted.

For about a century most manufacturing companies have used Standard Cost Accounting as their management accounting system to record transactions and produce financial statements. This system was developed in the early 1900s and is obsolete for today’s business environment both in general and specifically in the context of a Lean Strategy. Those companies that have discontinued it have substituted some form of Plain English financial statements. (See Real Numbers: Management Accounting in a Lean Organization). These statements are easier to understand by people that don’t have degrees in accounting and provide much more transparency into the working of the company.

Back to the opening sentence of this article…is it true that most companies have not adopted lean accounting? Unfortunately, there are no studies that I am aware of that definitively answer this question. However, the anecdotal evidence is that many companies that are pursuing a Lean Strategy have started to apply the concepts, principles and practices of Lean to their business and accounting processes. They see it as the logical extension of eliminating waste. However, the anecdotal evidence also is that very few companies have given up their standard cost accounting systems. This is unfortunate at best since the presentation of standard cost and variances doesn’t provide any useful information to management in an environment that is constantly changing. And at worst, it’s dangerous since it hides the real improvements that are taking place and can actually report them as negative events that can derail the company’s Lean efforts.

Why are financial executives so reluctant to abandon Standard Cost Accounting? My personal opinion is two fold. First, financial executives are, by nature, very uncomfortable with change. I have experienced this in conversations with many financial executives. They are reluctant to experiment with something “new”. I explain to them that I was also skeptical at the beginning. But I was so frustrated by the lack of useful information that the standard cost accounting financial statements provided that I was willing to experiment with running Plain English statements in parallel with standard cost accounting statement for over a year. In the end I was convinced that the Plain English statements provided much better transparency into the economics of our business and helped us see the results of the improvements that were taking place as we implemented our Lean Strategy. At that point abandoning Standard Cost Accounting was easy…intellectually. From that point on we relied on the Plain English statements and lean oriented metrics.

However, it did take a couple of years to untangle our systems from the standard cost structure, but those reports were not used anymore and never left the accounting department.

One last point…some proponents of Plain English financial statements do not believe that they need to conform to GAAP accounting. I do not agree with that. Although tax accounting financial statements do not conform to GAAP, no one outside of accounting sees them. However, everyone sees the public GAAP statements, and if the management accounting statements report different sales or profit numbers that can only create confusion…what is the “real number?”. Plain English financial statements can report the same revenue and profit as GAAP financial statements, but in a way that you can clearly see items that are merely GAAP requirements…e.g. capitalizing labor and overhead for goods produced but not sold.

How do we get from where we are to where we want to be? This year was the 15th annual session of the Lean Accounting Summit. Every year there are impressive presentations from companies that have adopted Lean Management Accounting. However, those companies are in the minority. Fifteen years ago those of us at the first Lean Accounting Summit believed that the combination of a good idea and hard work would change the management accounting landscape. The reality is that in spite of that belief, we have had to face the reality that getting financial executives to experiment, and then abandon standard cost accounting is more difficult than we expected. It is asking them to challenge what they were taught at the beginning of their accounting careers in college and practiced ever since.

So, the final question to those accounting professional reading this article is: Do you want to coast along doing what you have always done, even if it doesn’t contribute real value to your company, or are you brave enough to experiment with something different that will contribute to your company being more successful? And for those of you in the accounting academic world: Are you willing to take the risk of teaching that standard cost management accounting is obsolete and Lean Management Accounting is better suited to today’s business world? During the past fifteen years of attending, and speaking at the Lean Accounting Summit I have met accounting professors that are willing to teach the next generation of accountants that there is a better way. Until we get the accounting academic community to understand this, and remove obsolete methods of management accounting from the curriculum, we will continue to have an uphill battle.

On the other hand, it is encouraging to see the number of companies that have embraced Lean Management Accounting grow over the past fifteen years. The number of industries, beyond manufacturing, that now attend the Lean Accounting Summit and the enthusiasm that this next generation of accountants shows for experimenting with ideas beyond the traditional standard cost accounting model is encouraging. I believe this bodes well for the future as this generation moves into senior financial management positions. I also believe that with LEI bringing this subject into the broader discussion about Lean practices with its new Lean Accounting Learning and Practice section on its website, the non-accounting community will realize that they don’t have to remain frustrated by traditional management accounting. Hopefully, this will give them the information they need to have a meaningful discussion with their accounting partners about experimenting with alternatives that serve their business needs better.